Money 101 for College Students: What You Didn’t Learn in School

Financial Literacy for College Students: Why it matters

Dipping your toes into adulthood often comes with an overwhelming number of new responsibilities: time management, maintaining relationships, schoolwork and life balance, and, most importantly, managing money. It is essential for college students, often those who are living alone for the first time, to understand how to handle finances and navigate through adulthood. However, financial literacy remains one of the most neglected subjects in many students' education.

In this blog we dive into financial literacy topics and how they can be used to set up college students for success with their newfound real-world challenges. Our goal is to make this topic engaging, relatable, and most of all, useful.

Why Financial Literacy Matters for College Students

Lack of financial education

Across the world, financial literacy education is not a consistent part of the required high school curriculum. This leaves a large portion of students unprepared to properly and efficiently manage money. Without a strong educational foundation to this topic students are at risk for overspending, debt traps or misuse or damage to credit.

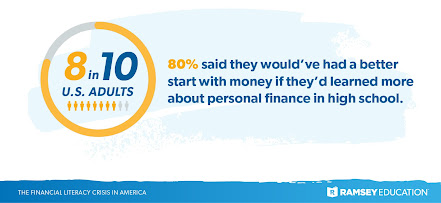

A study by Ramsey Solutions found in 2023 that 72% of U.S. adults have said that they would feel further ahead with their finances if they had personal finance education in high school. Learning financial basics can help prepare young adults today and potentially decrease the number of adults who feel behind due to lack of financial education.

Source: The Financial Literacy Crisis in America: 2023 Report - Ramsey

Managing money for the first time

College is often the first time that students:

Pay rent and utilities

Budget and pay for groceries and daily needs.

Apply for credit cards.

Establish credit

Take on student loans.

Without the proper guidance, these responsibilities can quickly become overwhelming and stressful. Financial literacy education can provide students with the tools, tips, and tricks to handle these responsibilities effectively and efficiently.

The risk of debt traps

Student loans, credit cards, and personal loans are often easily accessible to college students. Without a basic understanding of interest rates, repayment terms and conditions, explanations of the consequences of late or missed payments, and the impact they have on credit, it makes it easy for students to unknowingly fall into debt traps that will stay with them for years.

Learning how to read loan agreements and documents, develop repayment plans, and calculate interest rates are foundational skills that can help students avoid these common debt traps.

Key Financial Concepts Every Student Should Know

Let's break down some of the most important financial concepts in an easy-to-understand way!

Budgeting

A budget is a simple way to plan out the way you use your hard-earned money. Budgets can be 100% personalized in order to track any of your income and expenses.

Income can be

Loans

Job earnings

Allowance

Scholarships

Tips

Educational stipend

Expenses can be a bit more diverse from person to person. Some basic expenses are

Rent

Utilities

Groceries

Books/ School supplies

Weekend spending

Car note/insurance

Memberships/subscriptions

Gas/ Fuel

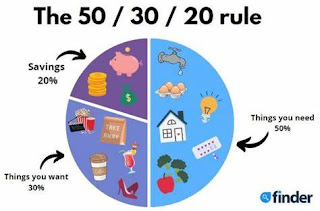

Tip: Try the 50/30/20 rule!

50% needs

30% wants

20% savings

Credit and Credit Scores

Credit scores reflect your trustworthiness to lenders within the financial world. You have better chances of getting approved for loans and leases/apartments the higher your score is.

Various factors can impact credit scores.

Payment History

Credit Utilization %

Credit history

Credit inquiries

To start building credit, students can open secured credit cards, take out credit builder loans, or even become an authorized user on a parent's account. To maintain good credit habits, it is extremely important to keep up with due dates in order to pay the bill on time, keep credit utilization below 30%, avoid opening multiple accounts at once, and regularly check and keep up with your credit status/report.

Many well-known credit card companies offer student-friendly applications that do not impact your credit score if you are not approved (commonly referred to as a "soft pull"). To apply, begin by researching reputable credit card companies that provide student credit cards with no hard applications. Once you have chosen, complete the application, providing all of the required information, and submit it to see if you qualify for a credit card they offer!

Savings and Emergency Funds

Even when the budget is tight, it is essential to set aside even a small amount of money to build a safety net. A good rule of thumb to start an emergency fund is to start with a small and manageable amount, such as $300-$500, and over time gradually set aside money to eventually be worth 3-6 months' worth of expenses. These funds can help with unexpected costs like car repairs or medical bills that aren't very predictable. Having this financial cushion can not only create a peace of mind, but it can also prevent you from having to rely on a credit card or loan in times of hardship or the unexpected. By regularly contributing to your emergency fund, you can develop healthy financial habits that will serve you well in the long run and set you up for success.

Student Loans

It is important to understand the difference between federal and private student loans before making the decision to borrow. Federal loans are offered by the government and often come with benefits like fixed interest rates, income-driven repayment plans, and the option to defer. Private loans, on the other hand, are provided by banks or financial institutions and often have variable rates and less flexible repayment options.

Take time to research your type of loan and prioritize your understanding of concepts like interest rates, the amount of time after graduation you have before your payments begin, what your future payments may look like, and ways to possibly pay it off early. For federal loans, you can find this information through resources like studentaid.gov or through your school's financial aid office. This same information for private loans can be found by communicating and asking questions with your bank or financial institution.

It is extremely important to understand that you should only borrow up to the amount you truly need for your tuition and other necessary expenses. Always remember that student loans are not free money and they must be paid back in accordance with the agreed terms and conditions. Staying informed about your loan, tuition expenses, and previous student debt can help to avoid overwhelming yourself with debt later on.

Try out these savings challenges by Fidelity!

The 52-Week Money Challenge:

As described by Fidelity, this challenge encourages budgeters to gradually increase their savings amount over the course of a year. For example, in week 1 save $1, in week 2 save $2, and so on until you reach week 52, saving $52. At the end of the challenge, you will have saved $1,378!

The No-Spend Challenge:

Fidelity's no-spend challenge involves choosing a specific time frame, like a specific week or month, where you commit to spending nothing on non-essential items like coffee, dining out, or random unnecessary purchases. Instead of spending the money, you would put it directly into savings. This is a very feasible way to cut unnecessary spending and reinforce good spending habits.

Source: 10 money savings challenges for 2025 | Fidelity

Benefits of Financial Literacy for College Students

Less stress and more control

Money is one of the biggest stressors for not only students but also many adults in general. Knowing how to properly manage your money or stay on top of your finances can reduce the anxiety that comes with it and increase confidence and security.

Smart financial decisions lead to a stronger future.

Whether it is saving money, avoiding debt traps, or building credit, making smart decisions that can start as early as college years can set students up for success well beyond their 20s.

Better academic performance or turnaround

Students who are financially stable are more likely to stay in school or perform better academically. As mentioned before, money is a huge stressor for students, and financial stress is a known leading cause for college dropout.

Independence

Understanding how money works gives students the freedom to make decisions independently about their own lives, goals, and priorities.

Final Thoughts

College is a time of growth, opportunity, and learning. It is also a time when poor financial decisions can leave lasting consequences for years. By focusing on financial literacy, students can take control of their present situations and secure a better future.

We believe every student deserves to understand their money and how it works. That's why we build spaces where financial literacy is not just talked about; it's taught and understood.

Follow along, join a challenge, and share your own financial journey with us and the people around you. Help us make financial literacy the new normal from the very beginning of adulthood!

We help college students take control of their finances through simple yet relatable content to build real-life financial skills.

By: Riley Delancy & Max VosburgReferences:

Fidelity: 10 money savings challenges for 2025 | Fidelity

Ramsey Solutions: The Financial Literacy Crisis in America: 2023 Report - Ramsey

Comments

Post a Comment